Analysis Nutanix wants be seen as a sexy software business and not a hardware appliance biz stuck with crap commodity hardware margins. So it is changing its business mode to position itself as a software-focused company.

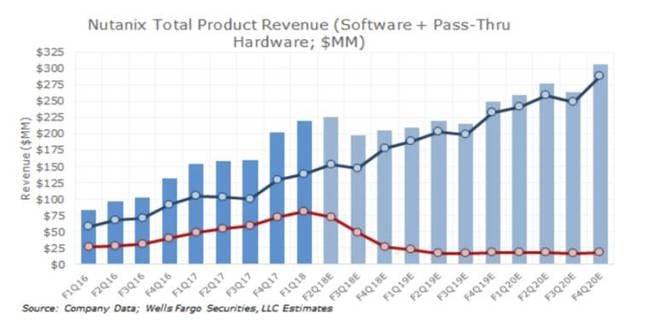

Senior Wells Fargo analyst Aaron Rakers said the hyper-converged firm “currently sells hardware and software products with its software running either on its own hardware or that of its channel partners. [Nutanix’s] first fiscal 2018 quarter’s hardware-only revenue totalled $80.4m, 29.3 per cent of total revenue. It was $48.8m a year ago.”

Nutanix’s hardware is contract-manufactured by Supermicro and Flextronics.

In the Nutanix’s most recent earnings call, company CEO Dheeraj Pandey said: “We are increasingly taking a software-centric approach to go-to-market and financial reporting.”

CFO Duston Williams added: “Today, we are software company, more specifically an enterprise cloud operating systems company, that up until now has delivered a majority of its software via its own branded appliance and recognise the associated hardware revenue. … This left many investors wondering, if we really are a software company or just another storage or appliance company.”

Part of the problem was that Nutanix recognised pass-through hardware revenues in its results.

So: “Going forward over time, Nutanix will emerge [as] exactly what it is: an enterprise cloud operating systems company,” meaning a software company.

He said: “We will begin the migration away from pass-through hardware related revenue. Beginning last quarter, we started the gradual migration related from recognising pass-through revenue, attributed to the hardware portion of our business.”

Currently “the hardware portion of our business is approximately 26 per cent of our total billings. This transition will come in two parts. First, with straightforward changes that will allow us to step aside for most hardware-only invoicing by enabling our legacy appliance manufactures to begin selling the NX hardware directly to our distributors. And secondly, by simply focusing on more software-only transactions, allowing our customers to them choose to run on a large number of server platforms.”

“We expect this transition to take a year or so and the result of elimination of at least 80 per cent of our pass-through hardware related revenue. All things being equal, the direct impact of this specific change would result in significantly higher software content and significantly higher gross margins with no change to our gross and gross profit dollars.”

Over time, Nutanix will start adding writeable Software-as-a-Service revenue with its Xi Cloud service offerings. Williams said: “Over time, we will start to position the company for increasing writable Software-as-a-Subscription revenue.”

There will be a Xi Cloud disaster recovery service launched in mid-2018 via a Google Cloud Platform partnership.

Starting in the third fiscal 2018 quarter, starting February 1, 2018; “We will start the process of compensating our sales teams on software-only related bookings. Once the change is fully implemented sales representatives will no longer be compensated for pass-through hardware sales.”

As a software business it compares itself favourably with other software and service companies such as Splunk, Netezza, Tableau and others in terms of size, growth and gross margins over the past year. That means being an $800 million shared software and support infrastructure company with gross margins above 80 per cent.

There will be channel changes, with Rakers noting Nutanix is working on “transitioning its distribution alignment for software-only sales, including the transition of its international distribution models from contracting directly with hundreds of individual resellers to contracting with a smaller number of larger global distributors”.

Rakers is modelling Nutanix’s hardware-only revenue decline to a sub-$20m/quarter level by the Jan 2019 quarter. He has said he believes its gross margin will grow from a mid/high-70 per cent range by the end of its fiscal 2018 to a low-80 per cent range by mid fiscal 2019. That should help profitability.

The change to a perceived software company could well lift Nutanix’s stock price, with investors favouring software companies over hardware ones. That could please investors and that, we think, is one aim of the shift away from hardware.

source:-.theregister.

{kind=link}

{kind=link}